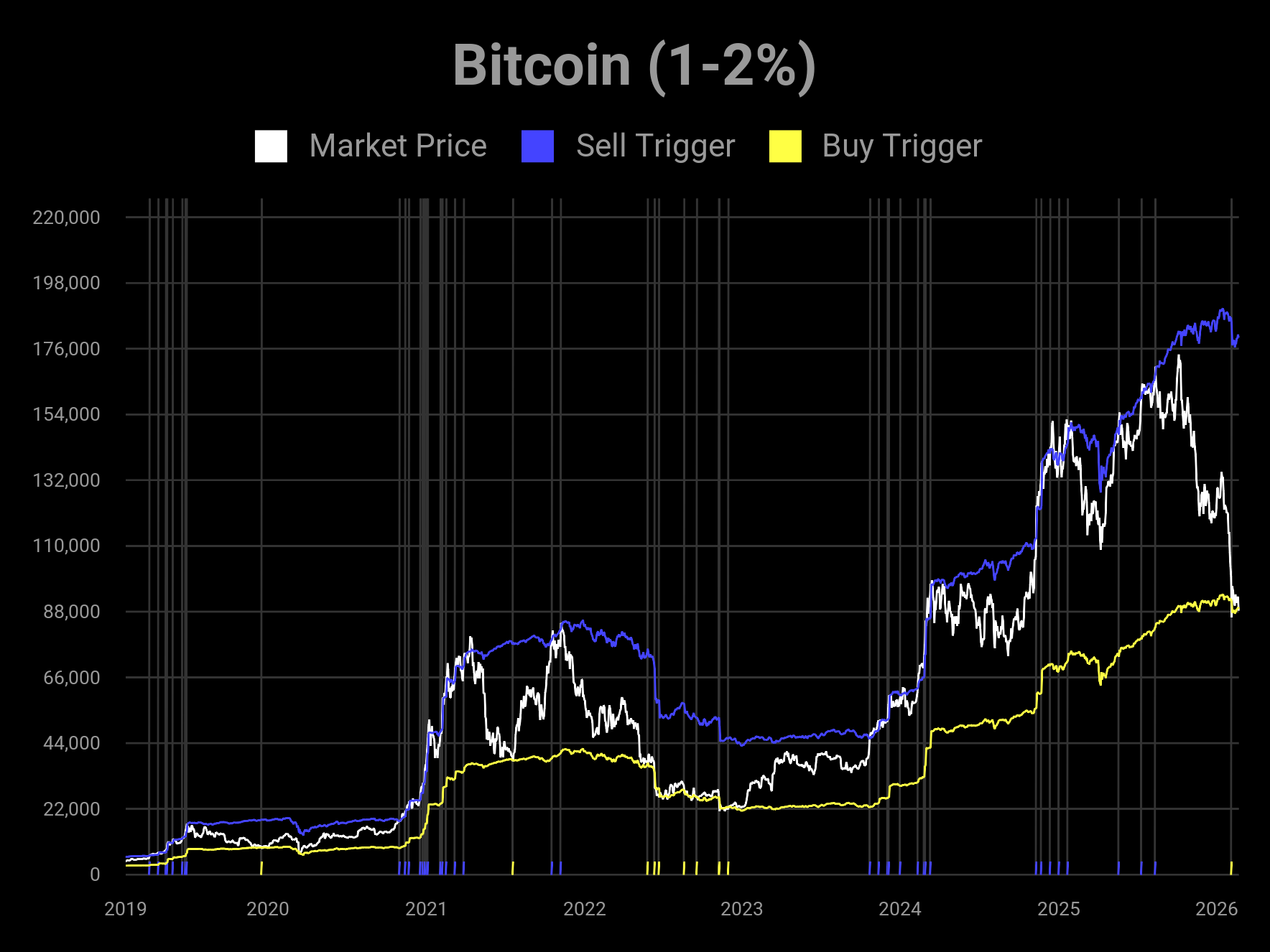

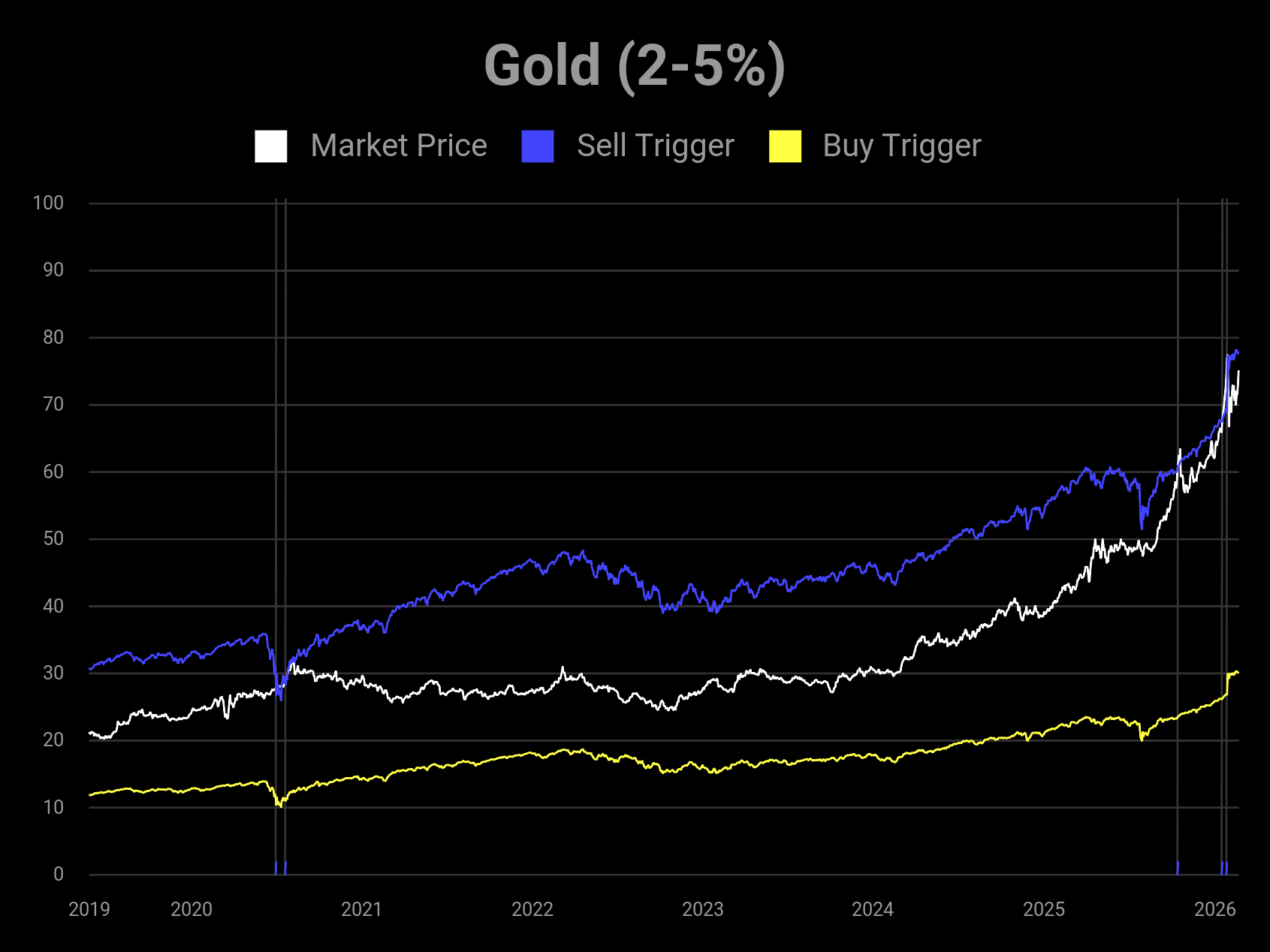

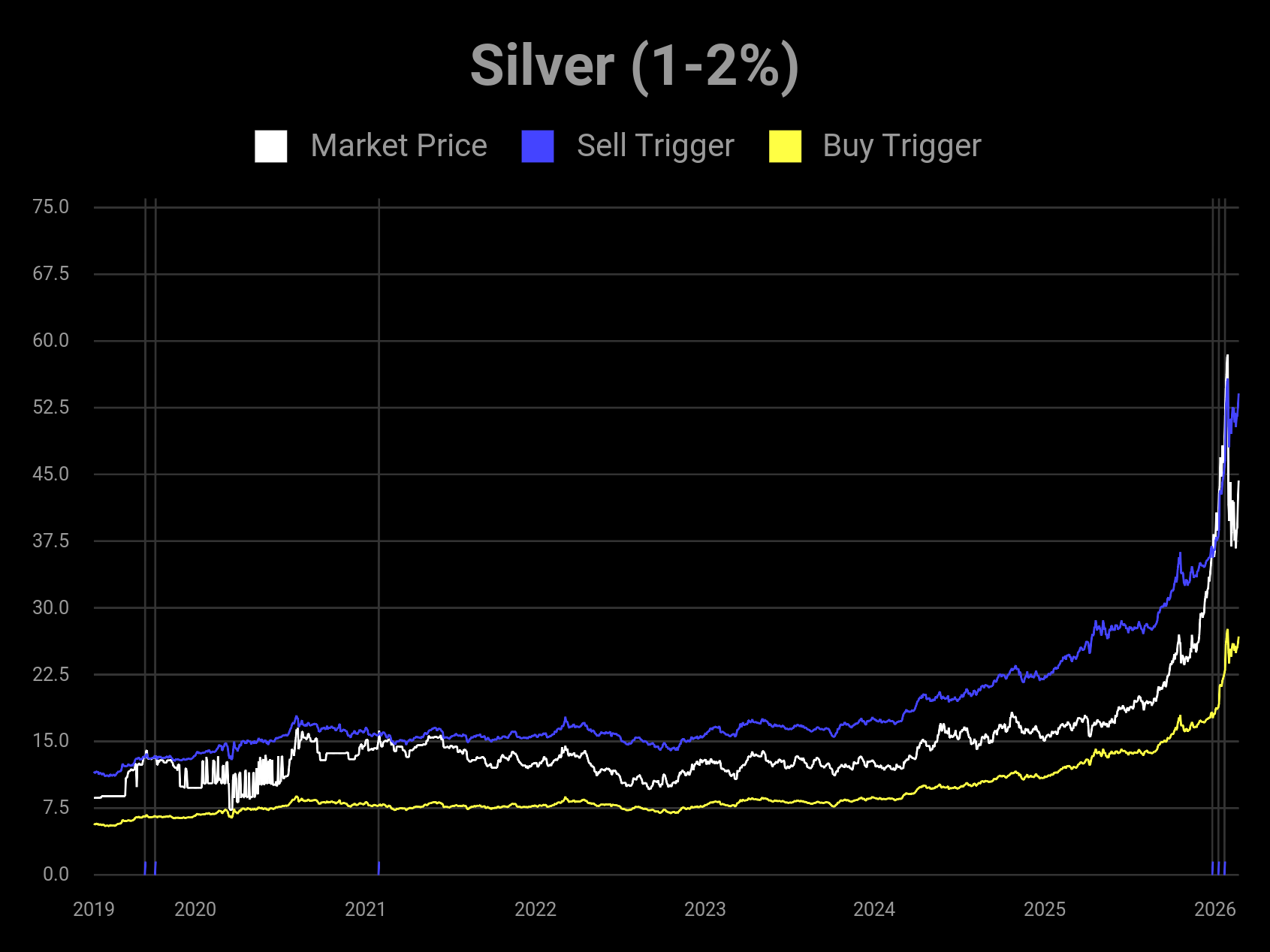

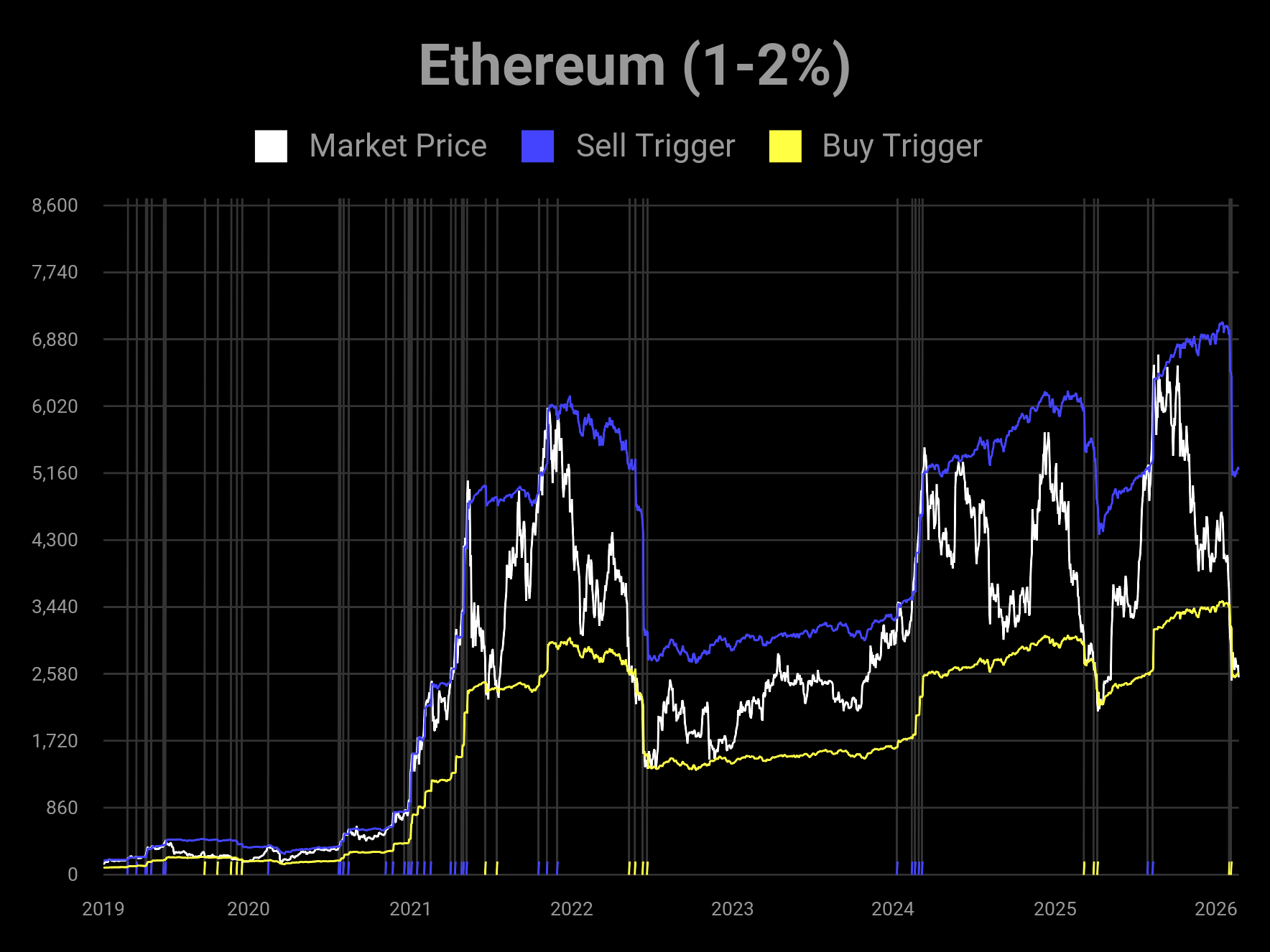

Passive Investing Models

The below charts simulate the purchases & sales of exemplary passive investors for various unproductive assets. The mechanical and disciplined rebalancing of passive investors can be viewed as a signal for the "regime" of the asset, as this strategy explicitly forces investors to sell into relative strength and buy during weakness.1 However, the purpose of this page is not to provide specific buy/sell targets, but to simply provide perspective if you are generally on-side with passive investors or not.

It requires both more skill and more luck to come out ahead if you are trading against disciplined passive investors.2 If you are buying while these charts say "sell", beware of your greed. If you are selling while these charts say "buy", beware of your fear.

These simulations are updated automatically at the end of every day based on realtime price data.

How does it work?

Each simulated investor holds two asset classes, the subject and the counterpart, at a desired allocation percentage. For example the chart titled Bitcoin (1-2%) means the investor wishes to hold 1-2% of their portfolio in Bitcoin and the remainder in Stocks. A globally diversified, market-weighted, home-biased index fund like VEQT is used as the stock counterpart. The investor uses a threshold based rebalancing strategy with a cooldown time of 1 week.

What is this NOT?

This is not a short-term trading reference. The buy & sell triggers are very far apart, generally spanning years. Meaning that you *must* be a long-term investor in these asset classes to use these signals. If you don't believe in the asset long-term, you won't find value in these models.

Additionally, the triggers are clustered. In other words: when a sell trigger happens, it is more likely to be followed by more sell triggers. This means these signals are not appropriate for entering or exiting the market at scale. Rather:

- A sell means passive investors are skimming profits, to reduce risk, but largely remain in the market.

- A buy means passive investors are adding small amounts to their position, to increase risk, but were largely already in the market.

What are the risks?

The idea of it being a good idea to hold unproductive assets in the first place is inherently biased into these models. If correlations with stocks are high and expected returns low, no amount of passive rebalancing will be sufficient to justify the strategy.3

Additionally, even after allowing an unproductive asset into the portfolio, the target allocation ranges are subjective and affect the outcome of the models. If instead a market capitalization weighted target is used to remove subjectivity, the rebalancing thresholds will move in proportion with the asset price, causing in turn rebalancing events to be rare or non-existant.4 Without rebalancing these simulations would produce no interesting results, so market-cap weights are ignored within the context of this page.

1: Scott Willenbrock, Diversification Return, Portfolio Rebalancing, and the Commodity Return Puzzle

2: EUGENE F. FAMA, KENNETH R. FRENCH, Luck versus Skill in the Cross-Section of Mutual Fund Returns

3: Harry Markowitz, PORTFOLIO SELECTION

4: Lisa Goldberg, Is Index Concentration an Inevitable Consequence of Market-Capitalization Weighting?